I hope that I am able to help other women in a similar circumstance by sharing my experience. Any time there is no cure, it is challenging to accept and manage. I found that by simply changing my diet, I could significantly improve my quality of life and regain who I was meant to be.

I am a woman suffering from Endometriosis. So what is it? Endometriosis is a disorder where tissue in the uterus abnormally grows in other areas of the body, such as your ovaries, lining, bowel and other areas of the pelvis. Endometriosis effects 1 in 10 women. You would think a disease this common would have more information and research. It’s challenging to find and there is no known cure. The misconception is that you just get cramping, headache, fatigue, etc. around your time of the month. Wrong! These words are understatements. My symptoms never stopped and caused me to seek specialized treatment at only 11 years old.

In 6th grade, I began experiencing extreme amounts of pain and would have abnormal periods. There was no timeline for when this would occur and doctors originally just chalked it up to me being so young and “developing.” I would regularly pass quarter sized blood clots/tissue, which is extremely painful to experience. I finally saw a pediatric specialist at Ann & Robert Lurie Children’s Hospital, who diagnosed me with PCOS (Polycystic Ovarian Syndrome). This disease causes cysts to develop on the ovaries, which can cause mild to severe pain. If they were small enough, you had to just let them develop and burst or dissolve by themselves. The only treatment option I had was to go on birth control at the age of 14.

I remember birth control being a blessing. It helped manage my symptoms and reduced the amount of bleeding I had. I felt like I could finally live a semi-normal life! However, that didn’t last very long. After about 6 months, my birth control prescriptions “stop working.” What I mean by this is that my body got used to the hormone levels and I would just get intermittent bleeding randomly throughout the month. I had no cycle control, which in turn increased my pain levels on a day to day basis. I went through this cycle of switching birth controls every 6 months for years.

Fast forward, I’m 21 years old. My symptoms have intensified over the last few years and I’m desperately seeking medical solutions to why I can’t get rid of my cramping and lower back pain. I was sleeping 9-12 hours a day and was still exhausted. I had started developing mild depression symptoms. I was struggling to maintain my weight and my periods were out of control again. Then all of a sudden they stopped all together. My doctors were convinced I was pregnant. They tested me multiple times to ensure I wasn’t having false negative tests. Yet, they all came back negative. Turns out I had a 2 inch x 2 inch cystic tumor on my ovary that had caused my period to stop completely. I was told that they would try to save my ovary in the surgery, but that they could not make any guarantees. I was terrified of what the outcome was. Little did I know I would be receiving an answer to a long awaited question.

My surgeon confirmed she was able to save my ovary and that she found something called Endometriosis. At this point she told me I was between stages 1-2 of the disease and that we were fortunate that they caught it early. She proceeded to explain that this could be why I experience such high levels of pain and that short and long term treatment options needed to be discussed. I was relieved to know what was wrong with me, but I had a false belief that things would improve. To the contrary, things only spiraled from here for me personally and with my health.

I complained post-op of a frequent intense pain in my side. She assured me it would reduce over time and might just be my body healing after the surgery. My doctor proceeded to tell me there was a possibility that I may have difficulty having children due to my disease. She didn’t think I was at a high risk of infertility then, but that if I waited until I was closer to my thirties, there was a higher likelihood that I could experience challenges. At the time, I was in a very serious relationship and she encouraged us to start a family as soon as possible. That was a lot to take in. I wasn’t ready for children, nor did I even want them in the next 5 years. I went into adult mode really quick. I felt a lot of pressure to get married and start a family. At the same time, it made me realize that I couldn’t rush things just because I might have a problem in the future. Ultimately, I had to ask questions that people at 21 don’t normally have to ask and make some tough decisions about my life and the people I kept in it.

In hopes of slowing the spread of my disease, I begin Lupron treatments. This medication puts you in a medically induced menopause. For those of you that have experienced menopause, you know what how horrendous this is. I took this treatment with no add back hormones, because they weren’t available at the time. After my first injection, I felt like I was dying almost immediately. I became super weak. I had intense hot flashes, my hair was falling out in large clumps, my body physically ached and my libido was so low that the thought of sex was nauseating. Then, the weight gain started. After 30 pounds of weight gain over three months, I had enough. I told my doctor that I felt worse on the treatment than I did without it and that I was done. She said I hadn’t been on the treatment long enough to get the full benefits of it and I could care less. To this day, I still deal with repercussions of that medication. I truly believe the joint and sciatic issues I experience are directly related to the side effects from the medication.

After I stopped the meds, I continued to complain to my doctor about the frequent pain in my side. It had developed into a stabbing pain during intercourse that was never there before. I had never really experienced excruciatingly painful sex at that point and thought it was a one time thing. Nope. Every time I had sex that stabbing pain was there. This is a symptom of endometriosis and could be related to the disease. However, I was also told that the scar tissue from saving my ovary could have resulted in some unintended effects to my body. Ultimately, I wish they would have just removed the ovary, because I’ve never been the same since. Intimacy became very challenging for me and this continues to be an issue. Even when the pain isn’t as prominent, you develop almost a PTSD response to sex. Prior to the pandemic, I was supposed to start pelvic wall therapy to help with managing and reducing this pain over time. It takes a very special partner to love you and support you unconditionally through this challenge.

Fast forward to 27. I’m living on my own and I’m dealing with my pain as best I can. I begin to start getting frequent infections and needed to see a doctor. My hormones were all out of whack and I couldn’t figure out what was wrong. I just knew that I was sick all of the time. My OBGYN had retired and I was searching for a new doctor. I began explaining my symptoms and the doctor I saw brushed them off like I was crazy. I chose to see a different doctor in the practice, who proceeded to tell me I was too young to have the issues I was describing and that they couldn’t possibly be hormone related. I told him that my symptoms correlated to the week of birth control I was on and that I only felt good during my placebo pills. He agreed with his colleague and told me that my issues weren’t related to the birth control I was taking. Four visits later, I was in tears, because my skin was so raw that I couldn’t function. Still, they couldn’t find anything wrong with me. I was tired of the doctors not listening to me, so once again I chose to see a third doctor in their practice. She was my saving grace. She listened to me, really listened. She told me to discontinue the use of the birth control and after some back and forth, were able to get my hormones under control.

Being off birth control was hard. I was experiencing endometriosis symptoms that I had never felt before. The pain was so bad that I began vomiting occasionally from the severe pain. I had constant headaches, abdominal and lower back pain. I was experiencing issues with my sciatic nerve in my right leg. The stabbing pains were the worst and would occur at random. I made it about 6 months without birth control before I went crawling back to my OBGYN begging for any kind of relief. We talked through my options and she recommended staying off the pill longer since my side effects were so severe. My choices were the depo shot or an IUD. Based on the side effects, I chose to take my chances with the IUD. I was told that my pain could increase for a short period of time, but that over the next few months, I should go back to normal. That may be the case for other people, but that was not my experience.

The 10 months that I had the IUD, my endometriosis symptoms were the worst they have ever been. I had so much sharp pain that l was having trouble getting out of bed and going to work. I couldn’t work out and I started to gain a large amount of weight again. I was under so much stress that I was having trouble functioning. I pushed through the pain and told myself it was temporary. It wasn’t. The pain increased and became scary. I began blacking out for very short periods of time. My endo-belly had gotten so bad that I had to buy pants 1-2 sizes larger just to wear during my flare-ups. Slowly the swollen/bloated feeling never went away. That was my norm. Distended stomach and all. My most terrifying moment was while I was driving home from work. I blacked out for a few seconds. It was brought on by a sharp stabbing pain that started while I was at a stop light. That was my last straw. I was fortunate that I didn’t get into an accident, but I knew I couldn’t live like this anymore.

I went back to the doctor and they scheduled an appointment to have the IUD removed, but I had to wait 8 weeks for the appointment. In the interim, my pain was so severe that I was hospitalized 4 weeks before my procedure. I suspected the IUD had punctured my uterus. To my surprise, they said my IUD was perfectly placed and that the symptoms I was experiencing was due to my endometriosis. I was told to take Motrin and go home to rest. Motrin. For anyone that lives with chronic pain, you know Motrin doesn’t do anything at all. I was beside myself and asked what more I could do to manage my pain. The ER doctor suggested talking to my OBGYN about a hysterectomy. I was 28 years old, in the ER, being told to consider a hysterectomy for a treatment option. I was appalled.

I still had four more weeks until I saw my doctor and by week two I was actually considering discussing surgical options like excision, ablation and even a hysterectomy. I was desperate for the pain to stop. I was angry at the world. I was angry at my body for imprisoning me to a hell that I felt like I could only understand. I hated my body, I hated the way I looked and I just really hated myself at that point. Things in my mind got darker than I’ll admit. It’s a part of myself I hope to never see again. I started watching all these videos from people who were suffering from Endometriosis. I was yearning for someone to relate to. I came across one person who said her eating habits really helped to make positive changes in her life. I frantically researched this topic and learned there is a correlation to gluten, soy and lactose intolerances and those suffering from endometriosis. I wasn’t sure if this was true, so I asked my doctor. She said that there are correlations, but that it’s not always helpful for patients suffering from the disease. Every person is different, so what may have helped others might not work for me. Since I was at a cross roads, she told me to go ahead and try eliminating those items to see if they could work.

It’s extremely hard to limit your diet, so I started by simply going gluten-free. Within a few weeks, I had noticed my inflammation had reduced and the pain I was feeling regularly was subsiding. I began to limit the amount of soy in my diet. Soy is very challenging, because it’s in everything. I do my best to eat soy free, but I do consume it occasionally. I started to notice my mood began to balance out and my bloating reduced. I had forgotten what it was like to not have pain every minute of the day. It was amazing to be able to make it through a whole day and not feel awful. Even my lower back pain had eased up. I went back on the birth control and to my surprise, I had absolutely no side effects that I had previously experienced. Could this all be because of a diet change?

In my gut, I know that the foods I eat impact how I feel. If I accidentally eat gluten or if I consume an Asian dish with gluten-free soy, I get cramping within a 12-24 hour period. Some people have asked me if the pain I feel is just because I had food sensitivities I wasn’t previously aware of. That answer is no. I still experience flare-ups where I have severe pain. However, they have greatly subsided in frequency and have been less intense since making these diet changes. I sincerely believe that my eating habits help to manage my chronic pain. It will never fully go away, but at least I have a fighting chance of better managing my symptoms! This was my way of telling endometriosis that it wouldn’t get the best of me! Moral of this story is, sometimes we seek medical advice and look for a treatment that’s a pill or a shot. We don’t always stop to consider if what we are eating has impacted our bodies negatively. My story shows the importance of food and eating well, because it can make a world of difference.

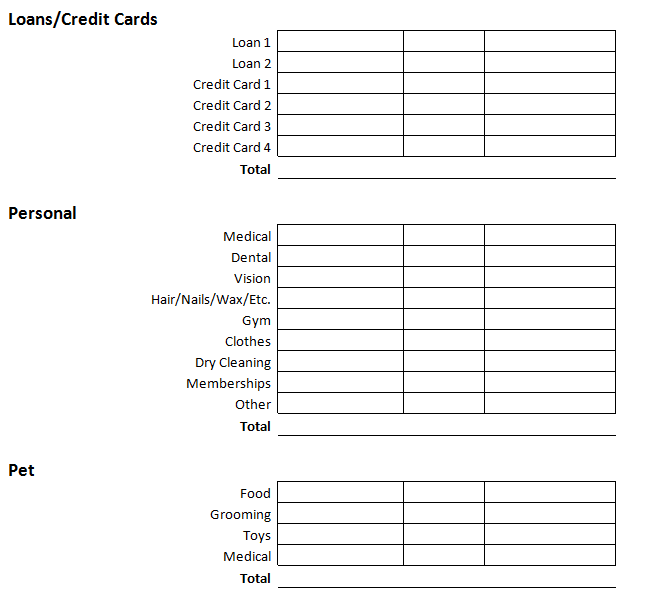

After I came to terms with the fact that my life was in financial disarray, I began researching different solutions online. Every source had different suggestions for ending the debt cycle, but I found that these 11 steps worked the best for me.

After I came to terms with the fact that my life was in financial disarray, I began researching different solutions online. Every source had different suggestions for ending the debt cycle, but I found that these 11 steps worked the best for me.