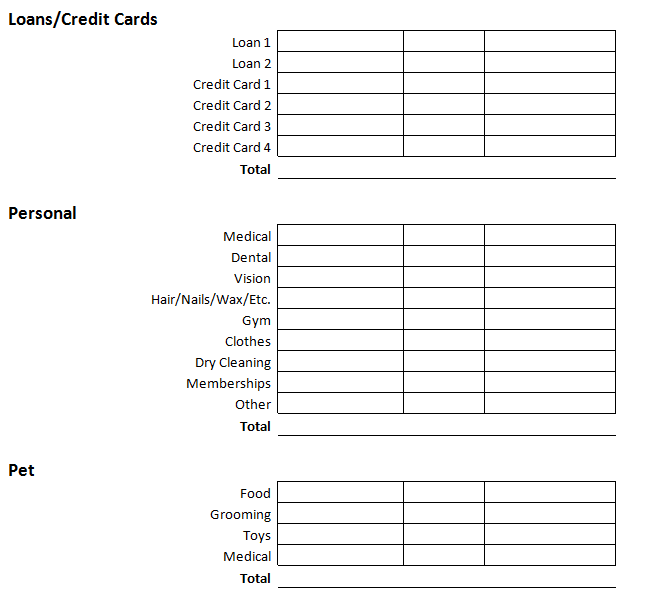

In one of my first posts, 11 Steps to Achieving Financial Freedom, I mentioned how tracking my expenses was a key component in creating my budget. I knew a budget would be necessary to meet my financial goals; but I made some mistakes along the way. My first month, I only factored in my fixed expenses. As you can imagine, I was completely off on my budget and it didn’t accomplish what I had hoped. I did some research and was able to correct the mistakes I made in my original budget. The following month was much more detailed and had me factor in items I really didn’t think about, like medical expenses. I’ve provided a basic example below so you can see how I plan my budget every month.

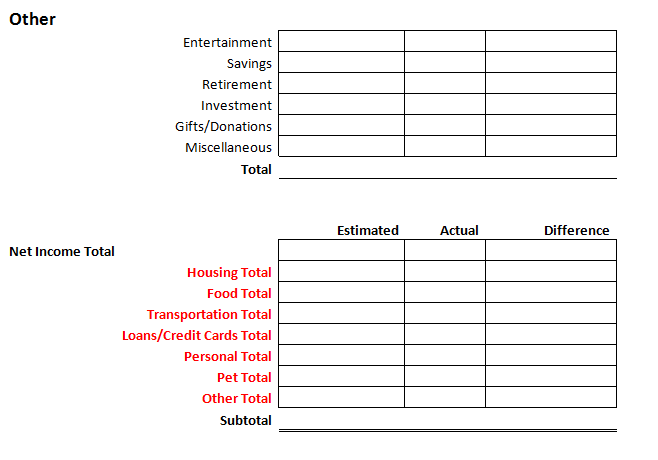

This Budget Plan does not factor in legal fees such as child support, alimony, etc. If you are self-employed and have to take out taxes and insurance expenses, I would suggest adding these categories to your budget. You’ll also notice I have a line item for “Entertainment” which I use for concert tickets, movies and media purchases. While I may not have a specific section for vacations, I tend to put my travel expenses into “Entertainment” as well. If you travel regularly, it may be beneficial to create a section just for your travel expenses too! The bottom table with all the totals was created to compare my expenses to my income. If there is money left over in a month, I make an additional payment toward my “focus” debt.

A few tips: Be sure to include expenses that may come up annually or quarterly. Last month, I completely left out my License Plate Renewal and my Quarterly Parking Permit expenses. This left me with a deficit of $231 in anticipated costs. I also didn’t include the gift I planned to give for a wedding. Boom! Now I was off on my budget by $331! I don’t care what anyone says, $331 is a large amount and can have devastating effects on your monthly payment schedule. For example, if I estimate that I have extra money, I may make a larger monthly payment than normal. If I do this while my budget is off, I run the risk of paying a bill late or not being able to pay cash for expenses I had budgeted. It is for these reasons that I am continuously adjusting my Budget Plan and make a new one monthly. That’s also why I only make the minimum payment at the time a bill is due and make additional payments at the end of the month. This helps me to avoid budgeting issues even if I miscalculate expenses. Next week I will be posting about debt repayment methods. This will help to explain why I make payments the way that I do and elaborate on “focus” debt.

I’d love to hear if this Budget Plan works for you! Please feel free to send comments and feedback!